Building a Valuation Practice: Staffing, Workflow, and Tooling

Most CPA firms stumble into valuation work rather than building it deliberately. Here is what a well-structured 409A and ASC 820 practice actually looks like, from your first hire to your first scalable workflow.

Key Takeaways

- check_circleA formal valuation policy document is the foundation of any defensible practice, covering methodology selection, data sources, and review cadence.

- check_circleThe question is not whether to hire a dedicated valuation analyst, but when: most firms need one before they hit five concurrent engagements.

- check_circleSeparating the roles of analyst, reviewer, and engagement manager prevents the single-point-of-failure problem that plagues small valuation teams.

- check_circleA written policy on 409A refresh triggers, including material events like priced rounds and major hires, protects both the firm and its clients.

- check_circlePurpose-built valuation software eliminates the manual reconciliation between cap table data and valuation models that consumes analyst hours in spreadsheet-based shops.

- check_circleAudit-defensible output requires documented methodology rationale, comparable company selection criteria, and a complete input change log, not just a final PDF.

Here is the thing about valuation practices at CPA firms: almost none of them were planned. A partner took on one 409A engagement as a favor to a startup client. That client referred two more. Before long, the firm has a dozen active engagements, a single analyst running every model in Excel, and a review process that lives entirely in one person's head. That is not a practice. That is a liability.

The question is not whether your firm should build a valuation practice deliberately. The question is how long you can afford to run an accidental one. This post covers the three pillars of a well-structured practice: staffing and role design, workflow and policy, and the tooling decisions that determine whether you scale or stall. If you are already thinking about the software side, the companion piece on moving from spreadsheets to purpose-built valuation software covers that transition in detail.

The Staffing Problem Most Firms Get Wrong

The most common staffing mistake is conflating the analyst role with the reviewer role. When the same person builds the model and signs off on it, you have no independent check on methodology selection, comparable company criteria, or Discount for Lack of Marketability (DLOM) inputs. That is not a documentation problem. It is an audit problem.

A functional valuation team has at least three distinct roles, even if some of them are part-time at first:

- Valuation analyst: builds and maintains the models, sources comparable company data, runs the equity allocation, and prepares the draft report.

- Reviewing manager: independently checks methodology rationale, comparable selection, DLOM inputs, and the allocation output. Should not be the analyst who built the model.

- Engagement manager: owns the client relationship, manages timing relative to grant dates and material events, and is accountable for delivery.

At low volume, one senior person can cover both the reviewer and engagement manager roles. But the analyst and reviewer should always be different people. The moment you compromise on that, you are one auditor question away from a difficult conversation.

When to Hire Your First Dedicated Analyst

The practical trigger for a first dedicated hire is somewhere around five concurrent engagements. Below that, a senior manager can absorb the analytical work alongside other responsibilities. Above it, turnaround times slip, review quality degrades, and the engagement manager starts doing analyst work to cover the gap. None of that is sustainable.

What to look for in a valuation analyst hire: familiarity with Discounted Cash Flow (DCF) and Guideline Public Company (GPC) methods, comfort with cap table mechanics (liquidation preferences, conversion ratios, option pool dynamics), and enough Excel fluency to spot a broken formula reference. The AICPA's Certified in Entity and Intangible Valuations (CEIV) credential and the ASA's Accredited Senior Appraiser designation are both signals of structured training, though neither is a prerequisite for a junior hire.

Building the Policy Foundation

A formal valuation policy document is the foundation of any defensible practice. It is the document that tells auditors, LPs, and clients that your firm has a consistent, transparent, and repeatable process, not just a collection of analyst judgment calls. Without it, every engagement is effectively a one-off, and your review process has no standard to measure against.

The policy should cover, at minimum:

- The specific valuation methods the firm will use for different types of engagements (e.g., GPC for late-stage companies with public comparables, Guideline Transaction Method (GTM) for early-stage companies with limited public data).

- The frequency of valuations for each client type, including the 12-month maximum interval for maintaining the IRS safe harbor on 409A engagements.

- The data sources the firm relies on for inputs and assumptions, including market data providers and financial databases.

- The review and approval chain, specifying who reviews what and what sign-off is required before a report is delivered.

- The definition of a material event that triggers an off-cycle valuation refresh.

Defining Material Events in Your Policy

This is where a lot of firms are vague, and vagueness creates client risk. A 409A valuation must be refreshed after any material event that could change the company's value. The policy should name specific examples so that both the engagement manager and the client know what triggers a call:

- A priced funding round (Series A, B, or later).

- A significant change in business model or pivot.

- A major acquisition or divestiture.

- A material change in financial performance relative to the prior valuation's projections.

Working with clients well in advance of anticipated grant dates helps avoid the timing gap that arises when a material event triggers an off-cycle valuation right before a planned option grant. That gap, where the old valuation has expired but the new one is not yet complete, is one of the more uncomfortable situations a valuation practice can find itself in.

What Good Workflow Design Looks Like

A well-designed valuation workflow has five stages, and the handoffs between them are where most practices lose time and introduce errors.

- Engagement intake: collect cap table data, financial statements, and client representations. Confirm the valuation date and the purpose (409A safe harbor, ASC 820 reporting, or other).

- Methodology selection: document the rationale for the chosen approach based on the company's stage, available market data, and the prior valuation's methodology. Changes from the prior approach need a written explanation.

- Model execution: run the enterprise value analysis, the equity allocation (Option Pricing Model (OPM), Current Value Method (CVM), or Common Stock Equivalent (CSE)), and the DLOM calculation.

- Independent review: the reviewer checks methodology rationale, comparable company selection, DLOM inputs, and the allocation output. All review comments are logged.

- Report delivery: the final report is delivered in a format that includes documented methodology rationale, comparable company criteria, and a complete input log.

The Review Stage Is Not Optional

Auditors reviewing 409A and ASC 820 work increasingly ask to see the review trail, not just the finished report. That means the review stage needs to produce a documented record: what was checked, what questions were raised, and how they were resolved. A comment in a shared document or a tracked change in a model is not sufficient. The review log should be a discrete artifact that travels with the engagement file.

The IRS's own business valuation guidelines require that all relevant activities be documented in the appraiser's workpapers, including planning, identification of relevant factors, and analysis. A practice that holds itself to that standard internally will have fewer surprises when a client's auditor comes asking.

Tooling: The Decision That Shapes Everything Else

Tooling is not just a technology decision. It is a workflow decision, a staffing decision, and a quality-control decision. The tools you choose determine how much of your analysts' time goes to analytical judgment versus manual data transfer, and how much of your review process is actually reviewable.

| Capability | Spreadsheet-Based Practice | Purpose-Built Platform |

|---|---|---|

| Cap table management | Separate file, manually synced to valuation model | Integrated module; equity structure flows directly into allocation |

| Methodology support | One model per tab, manual blending across approaches | DCF, GPC, GTM, Backsolve, and Post-Money with configurable weighting |

| Equity allocation | Custom OPM formulas, error-prone and hard to audit | OPM, CVM, and CSE with automated breakpoint calculations |

| DLOM calculation | Manual Chaffe/Finnerty inputs, no cross-check | Built-in models with documented inputs and output log |

| Review trail | Email chains and file timestamps | Timestamped change history tied to specific inputs and assumptions |

| Report generation | Manual formatting in Word or PDF | Structured report output with methodology rationale and comparable criteria |

| Multi-analyst collaboration | File sharing with merge conflicts | Role-based access with concurrent editing and permission controls |

The spreadsheet column in that table is not a caricature. It is the actual state of most small and mid-size valuation practices today. And it works, until it doesn't. A single broken formula reference in an OPM model can materially misstate the fair market value (FMV) of common stock without anyone catching it before the report goes out.

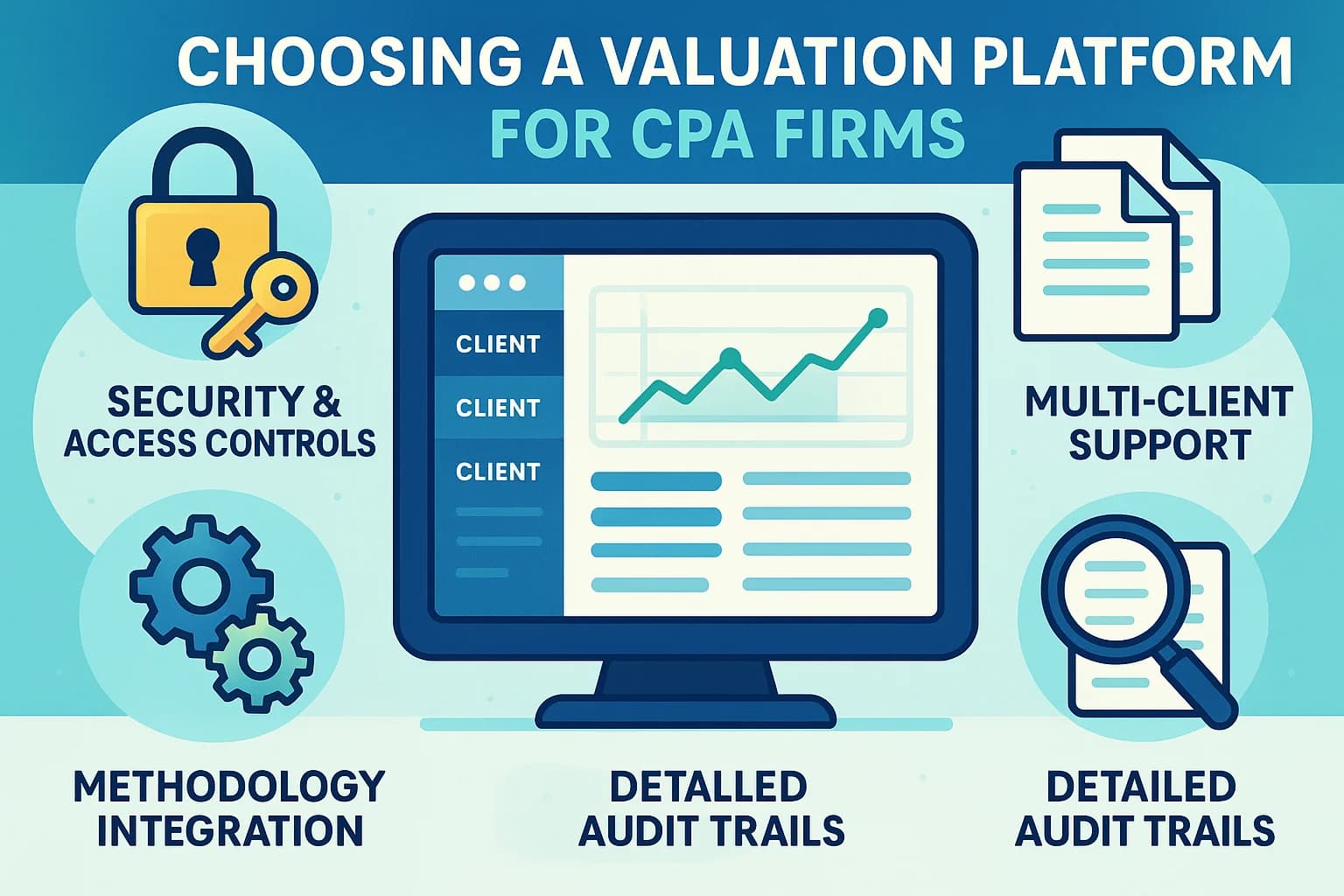

What to Evaluate When Choosing a Platform

Not every platform is built for CPA firm workflows. Some are designed for the company being valued, not the firm doing the valuing. When evaluating options, the questions that matter most are:

- Does the platform support multiple clients under a single firm account, with separate engagement files and access controls?

- Can the reviewer access the full input and assumption log, not just the final output?

- Does the platform support the full range of methodologies your practice uses, including weighted blending across enterprise value approaches?

- Is the cap table integrated with the valuation workflow, or are they separate modules that require manual reconciliation?

- What does the report output look like, and will it satisfy a Big 4 auditor reviewing the work?

Scaling Past the First Five Engagements

The first five engagements are manageable with almost any setup. The problems show up between five and fifteen, when the informal systems that worked at small scale start breaking down. Version control becomes a real issue. Turnaround times slip. The reviewing manager is spending more time reconstructing what the analyst did than actually reviewing it.

Scaling past that inflection point requires two things to happen at roughly the same time: a second analyst hire and a tooling upgrade. Doing one without the other tends to create new problems. A second analyst on a spreadsheet-based workflow doubles the version control risk. A platform upgrade without enough analyst capacity to use it properly just means paying for software that sits underused.

The ROI Case for Building It Right

Here is the thing about the upfront investment in staffing, policy, and tooling: it pays back in the places that are hardest to measure until they go wrong. Audit response time. Analyst turnover (because good analysts leave practices where they spend half their time on manual reconciliation). Client retention when a startup's auditor pushes back on a report and the firm can produce a complete, documented review trail in minutes rather than days.

The practices that grow their valuation revenue consistently are not the ones with the lowest per-engagement cost. They are the ones that can take on a new client at Series B, deliver a defensible report on a two-week timeline, and hand the auditor everything they need without a scramble. That capability is built deliberately, not accumulated by accident.

If your firm is at the point where the informal setup is starting to show its limits, the right time to redesign the practice is before the next audit cycle, not during it.

Frequently Asked Questions

How many staff do you need to start a 409A valuation practice?expand_more

There is no hard minimum, but most firms find that one dedicated analyst and one reviewing manager is the practical floor. Below that threshold, the analyst becomes the reviewer, which creates audit risk and limits throughput. As volume grows past five to eight concurrent engagements, a second analyst and a dedicated engagement coordinator become necessary to maintain turnaround times.

What should a valuation policy document include?expand_more

A valuation policy should specify the methodologies the firm will use for different asset types, the frequency of valuations, the data sources for inputs and assumptions, and the review and approval chain. It should also define what constitutes a material event that triggers an off-cycle valuation. This document is reviewed by auditors and LPs, so clarity and consistency matter as much as the content itself.

When does a 409A valuation need to be refreshed?expand_more

A 409A valuation must be refreshed at least every 12 months to maintain the IRS safe harbor. It also needs to be refreshed after any material event that could change the company's value, such as a priced funding round, a significant change in business model, or a major acquisition. Working with clients well in advance of anticipated grant dates helps avoid timing gaps.

What is the difference between fair value and fair market value in a valuation practice?expand_more

Fair market value is the IRS standard used in 409A valuations: the price at which property would change hands between a willing buyer and a willing seller, neither under compulsion. Fair value is the GAAP concept under ASC 820, defined as the price received to sell an asset in an orderly transaction between market participants. They overlap in spirit but are not interchangeable, and a well-run practice keeps them distinct in its documentation.

What tooling does a valuation practice actually need on day one?expand_more

On day one, a practice needs a cap table management system, a methodology execution environment that supports at least DCF and Guideline Public Company analysis, and a report generation workflow that produces audit-defensible output. Spreadsheets can technically handle all three, but they introduce version control and formula-error risk that becomes expensive to manage as volume grows. Purpose-built platforms address all three in a single workflow.

How do you structure the review process to maintain audit defensibility?expand_more

The reviewer should be someone other than the analyst who built the model. The review should cover methodology selection rationale, comparable company criteria, DLOM inputs, and the equity allocation output. Every review comment and resolution should be logged, not just the final approved version. Auditors increasingly ask to see the review trail, not just the finished report.

Run audit-ready valuations in one platform

DCF, GPC, backsolve, OPM/CVM, cap tables, built for CPA firms and valuation advisors. See a walkthrough tailored to your practice.